Have you ever wondered how investors can generate income while managing risk in a volatile stock market? The strategy of selling covered calls, especially understanding the “delta” aspect, offers a fascinating way to achieve this balance. This comprehensive guide is written to help you to uncover the secrets of leveraging covered call delta to potentially amplify your returns.

Understanding Delta : Stock vs Option Movement

Delta is a foundational concept in options trading, essential for both buyers and sellers of options. In the context of selling covered calls, delta serves as a measure of how much the price of an option is expected to change based on a $1 movement in the underlying asset’s price. Essentially, delta reflects the sensitivity of an option’s price relative to the stock it is tied to. For example, a call option with a delta of 0.5 indicates that for every $1 increase in the stock’s price, the call option will increase by approximately $0.50. This relationship helps covered call sellers estimate potential profitability or losses from shifts in the underlying stock price. It’s not just a theoretical number but a practical tool for predicting the option’s behavior in real-market conditions.

Beyond its role as a price predictor, delta provides insights into the probability aspects of options trading. Specifically, the delta value can be interpreted as the probability of the option expiring in the money.

For instance, a call option with a delta of 0.3 suggests there’s roughly a 30% chance that the option will be profitable at expiration, assuming no significant changes in volatility or time decay. This probability insight is instrumental for traders when selecting which options to sell, as it forms a basis for determining the likelihood of having to sell the underlying shares. Selling a call out of the money with a low delta means a lower chance of having your shares called away.

When it comes to selection criteria and risk measurement, delta acts as a critical component. In the case of covered calls, higher delta value indicates greater risk that it will end with intrinsic value. Lower delta means less chance of the option expiring with intrinsic value.

In contrast, selling a lower delta suggests less risk but also smaller profit opportunities, at least on the short side of a covered call. If you sold a call significantly above today’s price, you would collect less premium but there is less risk that your shares will be called away. On the other hand you could benefit from the share price rising.

Choosing the right delta involves balancing the desired level of income from selling the covered call with the acceptable level of risk in potentially having to sell the stock.

For instance, if your primary goal is to collect premiums without selling your shares, selecting an option with a delta closer to 0.2 might be a good idea. You have plenty of room for upside before you have to give up the shares.

However, if you’re open to parting with your shares for the right price, an option with a delta closer to 0.5 might offer better premium income and a higher probability of exercise. Understanding how delta works allows you to tailor your options trading strategies to match your financial goals and risk tolerance effectively. More on the maths of itm vs otm calls in this article.

Using Delta to Mirror 100 Shares

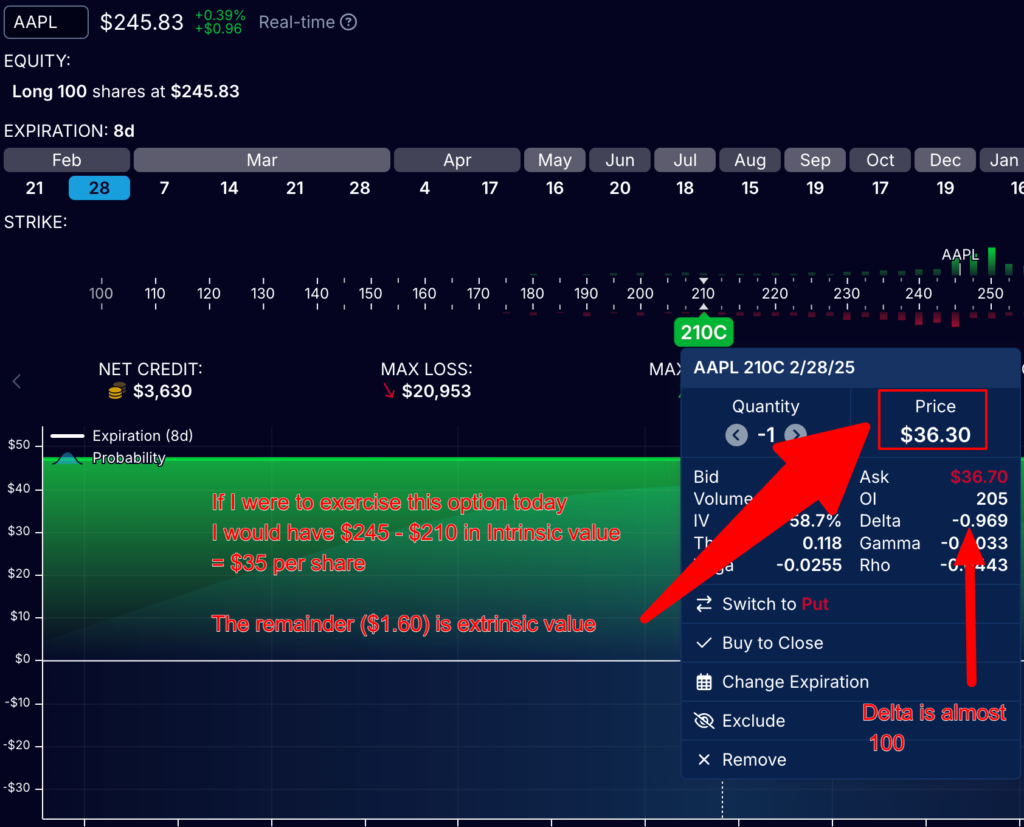

I explained earlier how Delta relates to the value of an option changing in relation to the stock price. That means essentially if your option has a delta of 1, every $1 movement of the stock affects the value of your option by $1.

This is particularly interesting since it provides a huge opportiunity : Stock replacement

What’s stock replacement?

Stock replacement basically means that you can replace holding 100 shares of a stock by a long call position. If you have a high delta, say 80 – 100, you can effectively mirror how shares would behave, without actually having to buy them. The catch? You have to pay a premium for the privilege — the “extrinsic” value.

For us this is interesting because – as Covered Call sellers – we need shares to sell calls against. But we can achieve the same thing by using a high delta call to emulate holding those 100 shares. We call this a synthetic position. These kinds of covered call trades are also called calendar trades or diagonals : you’re trading two options with different expiry dates.

In case you don’t already know about my trading strategy, it involves using this technique – using a synthetic position and selling weekly calls against it — and actually there are some simple rules that I follow to choose the delta.

Advanced Delta Strategies : Managing Portfolio Risk

One noteworthy approach is the multiple position approach, which involves holding a variety of option positions simultaneously to achieve a desired delta. This technique allows investors to fine-tune their market exposure more precisely.

For example, instead of simply purchasing call options to gain bullish exposure, traders can balance their positions with puts or other derivatives to hedge against potential losses.

Consider an investor who believes that a stock will rise but wants to mitigate risk. They might buy call options while also selling puts to collect premium income, achieving a balanced delta that aligns with their market predictions. Balancing delta this way adjusts your overall portfolio risk.

This is called portfolio delta management. The process involves regularly monitoring and adjusting the overall delta of a portfolio to maintain a consistent risk profile. In practice, this means that as the underlying asset’s price fluctuates, traders must evaluate their holdings and make adjustments to ensure their portfolio delta remains within targeted guidelines.

Let’s say the market takes a sharp turn, and your portfolio’s delta becomes more positive than intended due to a price increase of the underlying assets. To maintain balance, an investor might introduce additional options or adjust existing positions to counteract the shift. By continuously managing portfolio delta, investors can better navigate market volatility and protect their investments from unforeseen market changes.

Adjustment triggers and rolling guidelines are essential components in this strategic framework. Adjustment triggers act as predefined indicators that prompt a trader to modify their positions when certain conditions are met. For instance, an investor might decide to adjust their delta if the underlying asset moves by a specific percentage, ensuring that their portfolio remains aligned with their overall market outlook.

Meanwhile, rolling strategies are techniques traders employ to prolong the duration of an option position. This typically involves closing a current position and initiating a new one with a different expiration date or strike price. These approaches are especially valuable for investors seeking to enhance their strategies over time. Combined, these optimization techniques create a well-rounded approach that balances risk and reward, empowering investors to navigate market volatility with greater confidence.