Out-Of-The-Money vs In-The-Money Calls: Which Strategy Maximizes Your Returns? (2025 Guide)

Choosing the correct strike price selection is one of the most stumbling blocks in options trading. This crucial decision can make or break your trading success. In this comprehensive guide, I’ll break down the key differences between out-of-the-money (OTM) and in-the-money (ITM) calls, helping you make more informed trading decisions. After managing over 1,000 options trades, I’ve learned exactly when to use each strategy – and the mistakes you absolutely need to avoid!

TLDR Version : Selling in the money might seem counter-intuitive but can actually protect your downside. On the other hand, selling out of the money gives you upside potential, but more downside risk. As we say, “the risk is to the downside”.

Understanding OTM vs ITM Calls: The Basics

Let me break down selling ITM vs OTM calls based on my experience – this distinction completely changed how I approach options selling.

Most people start out selling OTM calls against their shares. Why? I think there are two psychological reasons for it. Firstly because they have a bias against giving their shares away. The trader doesn’t buy shares in stocks he generally doesn’t like, we have a bias of “buy and hold” mentality.

The second is that we know we want the option to expire worthless. The easiest way to think of it is if the option strike price is still above the share price at close. In other words, I sell a $50 call, and the stock ends at $48, my option will be worthless. We start to get worried when the share price goes above the strike price – for example, the underlying shares go up in value to $55, we would have a -$500 unrealised loss.

The reality of that scenario is however, that the value of the underlying will also go up.

If the price goes up to $55, our shares are now worth an extra $5 per share. So the $500 loss I encountered by letting my call go in the money was counteracted by the $500 gain in shares.

What remains is the extrinsic value – the time value or “juice”.

The advantage of selling this OTM call however, was that while I accepted a lower amount of premium, I left room for my underlying to make a gain. Let me break down what I mean with this example :

When you sell an ITM call, you’re actually selling something with real, built-in value right now. Here’s what I mean: Let’s say a stock is trading at $50, and you sell a $45 call. That option already $5 of intrinsic value baked into it ($50 – $45 = $5). You’ll collect a bigger premium upfront – maybe $7 total ($5 intrinsic value plus $2 time value) – but there’s a catch. At expiration, if the stock is still at $50, you’re going to have to buy that call back for at least $5.

On the other hand, if the value goes down to $45, then the $5 that was borrowed does not have to be repaid, as this intrinsic value is now $0. That means you get to keep the whole $7.

The catch? For premium sellers like us who are selling calls – we are selling calls against an underlying. In other words, we have 100 shares (or equivalent) that we’re selling calls against. If the price goes down to $45, we have lost $5 per share, or $500.

The good news is that this loss in value of the shares is covered by this ‘intrinsic value loss’ that the option we sold experienced. So, while we lost $500 on the shares, we gained $500 on the option. PLUS we also collected the $2 extrinsic value.

What happens when the share price goes up?

You stand to gain the most by selling an OTM call. If the price goes up, you gain on the underlying shares and get to keep all the premium so long as the price does not go above your strike price.

ATM and ITM perform well, but are less profitable. ATM will always have the highest amount of extrinsic value.

Let’s examine what happens,

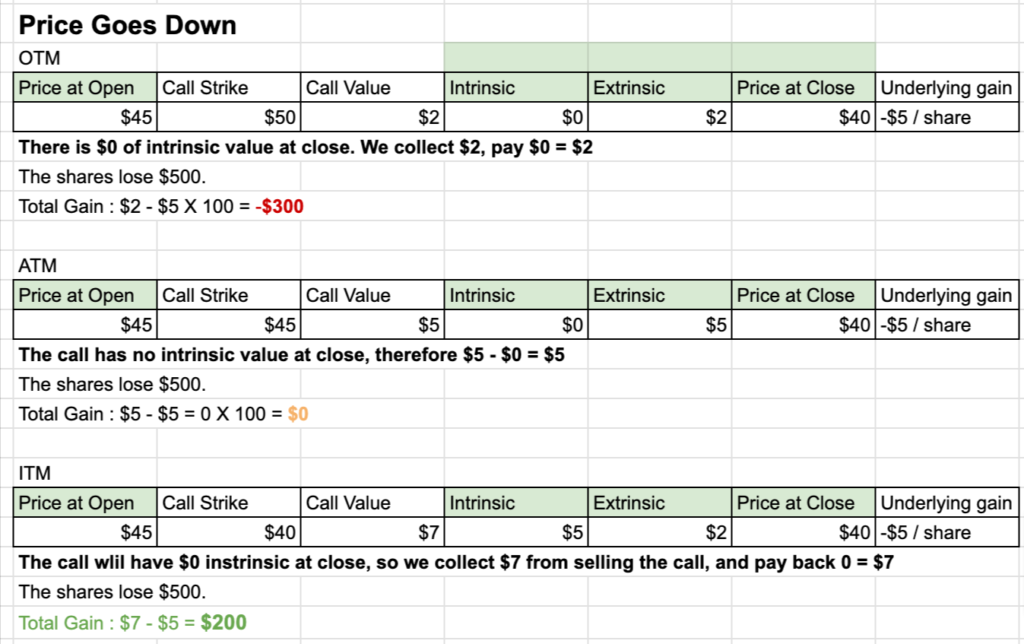

When the price goes down :

When the price goes down…

You will notice that the OTM call doesn’t perform very well. That’s because we lost so much value in the underlying stock. Sure, we got to keep all the premium from the short call, because it expired under the strike price. However, the losses on the underlying outweighed the gain on the short call.

ATM and ITM however, perform much better when this happens. Let’s see why.

At The Money calls give you the most extrinsic value. That means you get a good cushion either up or down – since the at the money premium was $5, that gave us a $5 cushion to the downside. So, although the shares lost $5 each, we collected $5/share from the covered call premium. The net result was $0. We broke even on the trade, even though the share price went down $5.

Here’s where it gets really interesting.

Selling an In The Money call when the price goes down gives us the best profit in this scenario. Why? Because we collected (or you could think of it as ‘borrowed’) some intrinsic value to begin with, when the price went down, we did not have to pay that back. We therefore get to keep all of the intrinsic and extrinsic value of the short call, which more than offsets the $5 loss we had in the shares. We lost $5 on the shares, but we got to keep $7 from the short call. The net result was a gain of $2/share, or $200.

When to use ITM / OTM / ATM?

You might be wondering, “but how do I know if the stock will go up or down?”, and the answer is – nobody knows. You might use some technical or fundamental analysis of where you think the stock is going to be at expiry and I’ve come up with some simple ideas in this post.

But the other way to think about it is this :

$200 was the lowest profit amount when the price went up. And it was the best profit amount when the price went down.

Why not work on the premise that you will usually gain $200 in INCOME per trade, so long as the price stays above a certain level. Yes, you will miss out on the gains you might make if you sell out of the money. But you will also have a higher probability of gains.

This is why we say, when you’re selling calls –the risk is to the downside. The risk is not to the upside where you lose on a short call that expires with intrinsic value – that is actually a good problem to have, because your underlying will have increased in value. The issue is when the stock moves down significantly.

Again, the risk is to the downside. If the shares move massively against you, your losses on the share price is going to be much greater if you sold an In The Money or At The Money call. In The Money calls give you greater protection against a downward move, but give lower yield.

So, to recap :

Selling OTM (Out of The Money) calls may seem the most logical way to approach covered calls, but selling ATM and ITM actually yield more consistent results and protect you from down-moves. When thinking about your strategy, make sure you consider the impact of the underlying that you’re selling calls against. You might consider employing a strategy to adjust when you decide to sell OTM or ITM, but over time – an In The Money strategy will yield the most consistent income.

Choosing between OTM and ITM calls doesn’t have to be overwhelming. Focus on your trading goals, risk tolerance, and market conditions. Start with paper trading to test both approaches, and always size your positions appropriately. Ready to implement these strategies? Begin with a small position and gradually scale up as you gain confidence.